Condo financing works differently from financing a single-family home, and most buyers find out why…

The Real Case for Homeownership Wealth Building

For decades, homeownership has been one of the most consistent wealth-building paths available to American households.

The typical homeowner has accumulated substantial housing wealth in recent years, while renters have generally not participated in that same asset growth.

Buying is not automatically the right move for everyone or at every stage of life.

Still, when someone is financially prepared to buy and can hold the property long enough, the advantages tend to compound over time through three core forces: equity, appreciation, and leverage.

💸 3 Engines Behind Homeownership Wealth Building

Housing costs money whether you rent or own, but a mortgage payment does more than cover the cost of living in the property.

1. Equity Through Principal Paydown

Part of each mortgage payment reduces the loan balance, and that reduction becomes equity.

Each month, a homeowner increases the share of the property they own outright, but a rent payment works differently.

Once the month ends, no ownership interest remains.

The payment benefited the landlord’s balance sheet, not the tenant’s.

2. Appreciation

Home values do not rise in a perfectly smooth line, and markets fluctuate across periods and regions.

Over long stretches of time, however, home prices have generally trended upward, and when that happens, the increase in value belongs to the owner.

3. Leverage

When someone buys a home with a down payment, they are controlling an asset worth far more than the cash initially invested.

If the property increases in value, the gain is based on the home’s full value, not just the down payment, which magnifies the wealth-building effect in a way most households do not replicate with other investments.

Together, these three forces explain why homeownership wealth building tends to outperform renting over long periods for people who can buy sustainably and stay put long enough for the math to work.

Renting and Buying Feel Similar but Results Differ

A renter and a homeowner both make monthly housing payments and may live in the same city, in similar homes, in comparable neighborhoods.

After 10, 20, or 30 years, the financial outcome often looks dramatically different.

A renter may have flexibility and fewer maintenance responsibilities, but years of rent payments do not create a housing asset.

In theory, a renter could invest the difference between what they pay in rent and what ownership would have cost, but most people do not do so consistently, and even those who do still miss the leverage built into real estate.

A homeowner is simultaneously paying for housing and building ownership in a long-term asset.

As the loan balance declines and the property value rises, the financial position strengthens.

That asset can eventually be:

- Sold

- Borrowed against

- Used to fund another purchase

- Passed on

The gap between renter and owner widens gradually, then meaningfully, then dramatically.

🔍 The Research on Long-Term Ownership

Research tied to the Wharton School through the National Bureau of Economic Research examined distressed borrowers during the Great Recession, including those who received mortgage modifications that helped them keep their homes and those who did not.

People who remained homeowners were much more likely to still own later on, and more than a decade after the recession, they had accumulated substantially more wealth than those who lost ownership.

The difference was large enough to amount to more than a full year of wages for many households.

Real estate wealth is less about timing and more about staying in long enough to recover from downturns and benefit from later appreciation.

That same research reflects an important limitation.

Homeownership is not universally better in every circumstance, and income can fall, home values can decline, and renting can be the better choice in certain situations.

For households that are ready to buy and capable of sustaining ownership over time, however, the financial outcomes have often been materially stronger.

Why Time in the Home Matters

Buying and selling a home is expensive, and when both sides of a transaction are accounted for, the cost typically runs around 8% to 10% of the property’s value.

Short-term ownership can weaken the benefits of homeownership wealth building because appreciation may not have had enough time to offset those costs.

National Association of Realtors data shows that older baby boomers typically stay in their homes for a median of 15 years before selling, and that long holding period helps explain why they have accumulated so much equity.

They gave appreciation time to compound, reduced their loan balances over many years, and made the costs of their original purchase relatively small compared to the total value they built.

Sustained ownership through multiple market conditions has often been more powerful than trying to time when to get in or out.

Refinancing as a Wealth Decision

Many people view refinancing through a single lens: can it lower the monthly payment?

When interest rates fall and a homeowner refinances into a lower rate, more of each future payment goes toward principal rather than interest, accelerating equity growth and improving the long-term results of homeownership wealth building.

Habitat for Humanity research found that households that missed the opportunity to refinance when rates dropped gave up meaningful wealth as a result.

When the numbers make sense, refinancing is a strategic wealth decision, not merely a cash-flow adjustment.

Costs, time horizon, and loan structure all matter, and when those factors align, the impact extends well beyond a lower monthly obligation.

⚖️ Home Equity Creates Options Renters Do Not Have

As homeowners build equity, they may gain access to borrowing tools tied to that equity, including a home equity line of credit or a home equity loan (HELOC), which allow owners to borrow against the value they have built without selling the property.

That flexibility can matter across a range of situations:

- Emergency expenses

- Major improvements or repairs

- Investment or business opportunities

- Bridging a financial transition

Wharton-related research noted that HELOC access fell sharply after the Great Recession as lending standards tightened.

Still, the broader point remains: homeowners with equity generally have more financial tools available than renters, and that additional optionality is a layer of homeownership wealth that many people overlook until they need it.

Homeownership wealth building works because it combines forced savings, long-term appreciation, and leverage into one recurring financial system tied to a place you already need to live. The biggest question is whether your finances, time horizon, and goals line up well enough to make it work for your specific situation.” — Wade Betz, Winning With Wade | Mortgage Education and Strategy

Tax Advantage Owners Do Not See Until They Sell

Under IRS rules for a primary residence, a homeowner may exclude up to $250,000 of capital gain from taxable income when selling, or up to $500,000 for married couples filing jointly, provided they meet the ownership and use requirements.

Generally, the property must have been owned and used as the primary residence for at least two of the five years before the sale.

This exclusion can apply to:

- Single-family homes

- Condominiums

- Co-ops

- Mobile homes

- Houseboats

—and if a homeowner lives in a property long enough for it to appreciate, a meaningful portion of that gain may be received free from federal capital gains tax.

Renters have no parallel benefit tied to monthly housing payments.

📝 Why Keeping Improvement Records Matters

A homeowner’s cost basis generally includes the purchase price plus qualifying capital improvements, and a higher basis reduces taxable gain at sale.

Additions, major renovations, new systems, and structural upgrades may increase basis, while routine maintenance generally does not.

Retaining documentation for major improvements is a wealth-protection strategy, not just a paperwork habit.

Wealth Building Extends Across Generations

Research cited by Habitat for Humanity found that children of homeowners tend to become homeowners earlier and at higher rates than children of renters.

The earlier someone enters ownership, the earlier the long compounding cycle of equity growth and appreciation begins.

Several factors contribute to that pattern:

- Homeownership provides a model that feels familiar and achievable

- Parents with housing wealth may be positioned to help with a down payment

- Families with ownership experience understand the process and face fewer practical barriers

When homeownership is absent from a family’s financial history, the path to ownership is harder, contributing to a widening wealth divide over time.

Homeownership wealth building can shape financial momentum for years beyond the original buyer.

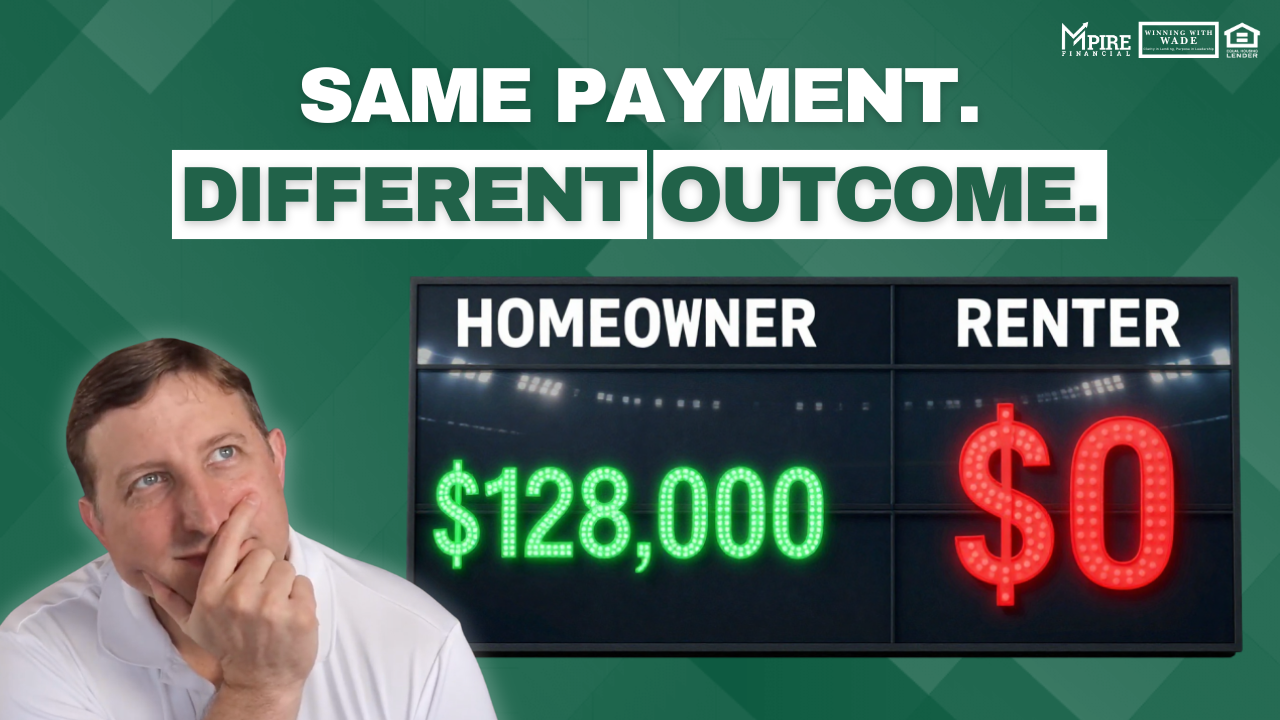

🏡 What the Current Market Is Showing

Recent National Association of Realtors data shows that the typical U.S. homeowner accumulated more than $128,000 in housing wealth over the last six years, and that gain was not distributed evenly.

Older generations, particularly baby boomers, have benefited from long ownership periods and multiple appreciation cycles, and many are now using accumulated equity to:

- Downsize

- Relocate

- Assist family members with home purchases

At the same time, the share of first-time buyers has fallen to its lowest point since NAR began tracking the metric in 1981, as affordability challenges and limited inventory have made the starting line harder to reach for younger buyers.

Those who already own continue to benefit from appreciation and equity growth, while those who do not own miss those gains and may face higher future entry costs if prices continue to compound.

The Cost of Waiting

People often assume the cost of waiting to buy is simply that homes may become more expensive, but that framing is incomplete.

Waiting also means:

- Not building equity during that time

- Not participating in market appreciation during that time

- Potentially trying to enter later against owners who have become even stronger financially

Many buyers who are succeeding right now are not waiting for ideal conditions.

Older millennials have leveraged equity from a first home to purchase the next one, while younger first-time buyers are using:

- Family support

- First-time buyer assistance programs

- FHA financing

- Other government-backed options with lower down payment requirements

They are finding a workable entry point and starting the clock on homeownership wealth building.

⏰ When Buying Makes Sense

Buying generally works best when income is stable enough to sustain ownership, the plan is to stay long enough to offset transaction costs, cash flow supports maintenance and ownership responsibilities, and the purchase fits within a realistic budget.

Renting may be the better option when:

- A job or location is likely to change soon

- Finances are too tight to take on the risks of ownership

- The time horizon is too short

- Flexibility matters more than wealth accumulation

The point is not that every person should buy immediately.

When buying is sustainable, homeownership wealth building has consistently produced meaningful long-term advantages.

Homeownership Wealth Building Checklist

Before deciding whether to buy:

- Assess income stability and long-term job outlook

- Estimate how long you realistically plan to stay in the area

- Calculate the full cost of ownership including maintenance and transaction costs

- Understand how equity, appreciation, and leverage work together over time

- Explore first-time buyer programs, FHA financing, and down payment assistance if needed

- Consider whether the entry point available today starts the wealth-building clock sooner than waiting

📣 Frequently Asked Questions (FAQs)

Why is homeownership considered more powerful than renting for wealth building?

A homeowner may build equity through principal paydown, benefit from appreciation, and use leverage on a large asset. At the same time, rent payments cover housing costs but generally do not create ownership in the property.

Does homeownership guarantee profit?

No. Home values can decline, transaction costs are significant, and the benefits are most meaningful when ownership is sustained long enough for appreciation and equity growth to outweigh those costs.

How long should someone plan to stay for homeownership wealth building to make sense?

Staying longer is generally better because buying and selling costs are high. Short-term ownership reduces the financial advantage significantly, while long-term ownership gives appreciation and principal reduction more time to compound.

How does refinancing affect homeownership wealth building?

When refinancing lowers the interest rate and the overall structure makes sense, more of each payment may go toward principal instead of interest, which can accelerate equity growth and improve long-term wealth outcomes.

What tax benefit supports homeownership wealth building?

Eligible homeowners may exclude up to $250,000 of capital gain from the sale of a primary residence, or up to $500,000 for married couples filing jointly, if they meet the ownership and use requirements, potentially making a substantial portion of the appreciation effectively tax-free.

Why does waiting to buy make homeownership wealth building harder later?

Waiting means missing years of equity growth and appreciation while existing homeowners continue to build both, which can raise the future barrier to entry and widen the gap between owners and non-owners over time.

About the Author

Wade Betz

Mortgage Broker at Winning WIth Wade · NMLS #280613

Wade has been a stalwart in the mortgage industry since 2006, dedicating himself to helping thousands of families navigate the complexities of home financing. With so much experience, he stands out as a leading mortgage originator in the Dallas-Fort Worth area.

Specializes in: DSCR Loans, VA Loans, Reverse Mortgages

Licensed in: AL, AZ, AR, CA, CO, CT, FL, GA, ID, IL, IN, KS, LA, MD, MI, MS, MT, NE, NJ, NM, NC, OH, OK, OR, PA, SC, TN, TX, VA, WA, WI

Related Posts